Asset Protection and Liability Shielding

For international entrepreneurs and global business owners, starting a business in the United States is a significant step toward expanding operations, raising venture capital, and accessing global payment networks. Can a non-US resident form a US LLC? Yes, non-US residents can form a US LLC 100% remotely without visiting the US or having a US Social Security Number. Do they owe US taxes? If the business has no physical presence, no US employees, and does not perform services physically in the US (i.e. non-ETBUS), and is a single-member disregarded entity, it pays 0% US income tax, though it must file annual information reports (Forms 5472 and 1120 pro-forma) to the IRS. Favorable states for formation are Wyoming, New Mexico, Delaware, or Florida depending on business goals. Disclaimer: this topic may change based on state, service provider, and current regulations.

Operating a business exposes owners to legal liabilities and financial risks. Choosing the right corporate entity is the most critical decision a founder makes. The Limited Liability Company (LLC) is the gold standard for global freelancers, e-commerce sellers, and software creators due to its unique combination of corporate asset protection, flexible management, and tax simplicity. It offers a shield against personal liability while maintaining a low administrative burden. Understanding the mechanics of asset protection and how to legally separate personal affairs from corporate activities is essential to securing your business operations.

The Separation of Personal and Business Liabilities

The primary advantage of forming a US LLC is the creation of a strong legal shield that separates your personal assets from your business liabilities. Under US corporate law, an LLC is recognized as a distinct legal entity. This means the company owns the assets, signs contracts, incurs debts, and holds liability—not the individual owners (referred to as members). If the company faces a lawsuit from a client or default on a merchant account debt, only the assets owned by the LLC are at risk. Your personal bank accounts, real estate, vehicles, and personal savings remain legally protected. This separation is recognized across all US jurisdictions, meaning a lawsuit filed in a state court against the business cannot target the member's personal wealth, provided the entity has been maintained correctly.

To establish this separation, the LLC must act as an independent economic actor. It must enter into contracts using its own legal name, possess its own tax identification numbers, and maintain its own financial records. When you sign a contract on behalf of your LLC, you must sign as a "Member" or "Manager" rather than in your personal capacity. This signals to the counterparty that they are dealing with a limited liability entity, not you as an individual. Failure to maintain this distinction in daily operations can lead to legal vulnerabilities and weaken the protection offered by the corporate structure.

The Risk of Piercing the Corporate Veil

While the asset shield of an LLC is robust, it is not automatic or indestructible. Under certain circumstances, US courts can bypass the liability protection and hold the members personally liable for the company's debts. This legal action is known as "piercing the corporate veil." When a court pierces the veil, it treats the owners and the business as a single entity, exposing personal savings, homes, and assets to the creditors of the LLC. To prevent this risk, international founders must adhere to strict corporate compliance standards and demonstrate that the LLC is a separate entity rather than a mere "alter ego" of the owner. Courts examine several factors when deciding whether to pierce the corporate veil:

- Separate Personal and Business Funds: You must never co-mingle personal money with LLC capital. Every dollar of revenue earned by the company must flow directly into a dedicated corporate bank account. Paying for personal expenses with a business card, or depositing client payments into a personal account, can destroy the liability protection. This is the most common reason courts pierce the corporate veil.

- Adequate Capitalization: The LLC must have sufficient capital to cover its initial setup costs and ordinary operational expenses. Underfunding a company to avoid paying creditors or leaving the company with zero assets while incurring large liabilities is viewed by courts as fraudulent. The LLC should maintain enough reserves to handle standard business risks and foreseeable debts.

- Clear Corporate Formalities: Even as a single-member LLC, you must sign agreements and act in the name of the company. All business invoices, contracts, and websites must clearly show the legal name of the LLC (e.g., "Company Name LLC") and use corporate signatures. You must maintain organized records of all major business decisions, such as opening bank accounts, entering leases, or purchasing assets.

- Internal Governance and Documentation: The presence of an Operating Agreement is a key piece of evidence showing that the LLC is structured and operated under formal rules. Although single-member LLCs do not have partners, having a signed Operating Agreement on file shows that the owner respects the corporate form and operates the business according to established legal protocols.

Maintaining the corporate veil is an ongoing process that requires constant vigilance. It involves keeping meticulous financial records, ensuring all corporate documents are kept up to date, and refusing to treat the company's bank account as a personal piggy bank. By establishing clear boundaries between personal finances and business operations, global founders can ensure that the liability shield remains fully intact, providing the peace of mind needed to scale their businesses globally.

Wyoming Delaware Florida and New Mexico State Comparison

Choosing the correct state of formation is the next major decision. Because the US does not have a single federal registry for company formation, companies are registered at the state level under state law. Different states offer different tax rates, annual fees, and privacy protections. For non-residents, the top four options are Wyoming, Delaware, Florida, and New Mexico. Each state caters to different business models, operational needs, and long-term financial budgets. Making an informed choice prevents expensive relocation costs later. Disclaimer: this topic may change based on state, service provider, and current regulations.

Wyoming: The Best Choice for Small Businesses and E-commerce

Wyoming is widely recognized as the most cost-effective and privacy-friendly state for bootstrapped founders, freelancers, and e-commerce sellers. Wyoming has low state fees ($62 annual report filing fee) and offers excellent privacy, as the names of the LLC members and managers are not published on the public database. This allows founders to protect their personal identity from public searches and marketing lists. Wyoming also has strong statutory protections for single-member LLCs, making it the default recommendation for solo founders. The state's judicial system is business-friendly, and its commercial laws are simple, making it easy to manage without expensive legal counsel. The state does not impose state corporate or personal income taxes, which means that for non-resident owners with non-US source income, state tax liability is absolute zero.

Delaware: The VC-Backed Startup Standard

Delaware is the corporate capital of the world, hosting over 60% of Fortune 500 companies. If you plan to raise venture capital from US institutional investors, issue stock options to employees, or eventually go public, Delaware is the required route. VC firms and institutional investors generally refuse to invest in entities formed outside Delaware due to the state's highly sophisticated corporate legal environment. Delaware features a specialized court, the Court of Chancery, which hears only business disputes and uses judges instead of juries, resulting in predictable and swift legal outcomes. However, Delaware is expensive, featuring a flat $300 annual franchise tax and registration requirements. It is also more complex, as its corporate laws are geared toward C-Corporations and active investment structures rather than small, remote LLCs. For bootstrapped businesses or solo e-commerce sellers, Delaware is rarely the most efficient path.

Florida: Ideal for Physical Presence or Active Trade

Florida offers a massive consumer market, geographical proximity to Latin America, and excellent local banking infrastructure. It is a solid choice if you plan to operate physical offices, warehouses, or hire employees in the state. Many international sellers choose Florida when setting up physical logistics centers. However, Florida lacks membership privacy, as all members and managers are listed publicly on the state database. Anyone can search the Sunbiz registry and find the names and addresses of the company's owners. It also features a high annual report fee of $138.75, which must be paid by May 1st each year. Late filings are hit with an immediate and non-negotiable $400 penalty. This makes Florida less suitable for remote digital nomads who want privacy and low administrative maintenance.

New Mexico: The Hidden Gem for Bootstrapped Founders

New Mexico is a highly attractive option that is often overlooked. It is the only US state that offers a combination of complete member privacy and zero annual state fees. When you form a New Mexico LLC, your name is not listed on the public registry, similar to Wyoming. However, unlike Wyoming, Delaware, and Florida, New Mexico does not require you to file an annual report or pay an annual franchise fee to the state. Your annual state maintenance cost is exactly zero. This makes New Mexico the absolute best state for bootstrapped founders, lean startups, or those who want to maintain an inactive entity for future use without recurring state costs. The initial filing fee is also low, at just $50. The only recurring cost you will have is your registered agent fee. This allows you to run a fully legal US business entity for a fraction of the cost of other states.

| Feature / Fee | Wyoming LLC | Delaware LLC | Florida LLC | New Mexico LLC |

|---|---|---|---|---|

| Initial State Filing Fee | $100 (plus convenience fees) | $90 (plus filing fees) | $125 (total state fee) | $50 (sabit devlet harcı) |

| Annual State Fee | $62 / year | $300 / year (Franchise Tax) | $138.75 / year | $0 / year (No annual fee) |

| Annual Report Required | Yes (Due on anniversary month) | No (Franchise Tax filing only) | Yes (Due by May 1st) | No (No annual report required) |

| Member Privacy | Yes (Names not on public record) | Yes (Names not on public record) | No (Publicly listed on Sunbiz) | Yes (Names not on public record) |

| State Income Tax | 0% | 0% (if no local operations) | 0% (for individuals/disregarded) | 0% (for individuals/disregarded) |

| Best Fit For | E-commerce, freelancers, solo founders | Startups seeking venture capital | Businesses with US physical operations | Bootstrapped startups, lean budgets |

Articles of Organization and State Publication Requirements

The formal legal creation of an LLC begins with the submission of the Articles of Organization (also referred to as the Certificate of Formation) to the state's Secretary of State office. This document contains the essential parameters of your business and must be completed with precise details. Once approved, the document acts as your company's legal birth certificate, allowing you to obtain federal tax IDs and establish financial operations. Disclaimer: this topic may change based on state, service provider, and current regulations.

Key Components of the Articles of Organization

When drafting your state filing, you must specify the following statutory elements:

- Legal Business Name: The name of your LLC must include a legal designator indicating its business structure (e.g., "LLC," "L.L.C.," or "Limited Liability Company"). The name must be completely unique and cannot conflict with any existing corporate entity registered in that state. Most states have online search tools where you can verify name availability before submitting the filing.

- Registered Agent and Address: You must appoint a registered agent physically located in the state of formation to receive official legal notices, service of process, and state correspondence. The agent's address is listed as the registered office of the LLC. Since non-residents do not reside in the US, hiring a professional registered agent service is required. The agent must be open during standard business hours to accept legal documents.

- Management Structure: You must choose between a member-managed structure (where the owners run daily operations) or a manager-managed structure (where designated managers govern the company). For most solo founders, member-managed is the default. If you have passive investors who will not participate in operations, manager-managed is preferred.

- Purpose and Duration: Most states accept a general purpose statement (e.g., "to engage in any lawful business activity") and list the duration of the LLC as perpetual, meaning it will exist until formally dissolved.

State Publication Requirements in New York and Nebraska

While states like Wyoming and New Mexico make LLC filing simple and inexpensive, certain states impose heavy administrative and financial burdens. A primary example is the publication requirement in New York and Nebraska. Under Section 206 of the New York Limited Liability Company Law, a newly formed NY LLC must publish a copy of its Articles of Organization or a notice of its formation in two newspapers once a week for six consecutive weeks. These newspapers must be designated by the county clerk of the county where the LLC's principal office is located. One newspaper must be weekly and the other must be daily. After the six weeks of publication, the newspapers will issue affidavits of publication. The LLC must then file a Certificate of Publication along with a $50 filing fee to the New York Department of State. The cost of publishing in counties like New York County (Manhattan) is extremely high, ranging from $600 to $1,500 depending on the newspapers designated. Failure to complete the publication requirement within 120 days of the LLC's formation results in the automatic suspension of the LLC's authority to carry on, conduct, or transact any business in the state of New York.

Similarly, Nebraska law (Section 21-117) requires a newly formed LLC to publish a notice of organization in a legal newspaper of general circulation in the county of its principal office. This notice must run once a week for three consecutive weeks. The notice must contain details such as the company name, address, registered agent, and nature of the business. Proof of publication (an affidavit from the newspaper publisher) must then be filed with the Nebraska Secretary of State. Failing to meet this requirement can invalidate the liability shield of the LLC. For global founders, these publication requirements are a major financial drain and logistically difficult to coordinate from abroad. Therefore, it is highly recommended that non-residents avoid registering LLCs in New York or Nebraska unless they have active, local brick-and-mortar operations in those states. States like Wyoming, New Mexico, and Delaware have no publication requirements, making them much faster and cheaper options.

Name Spelling Alignment for Banking and Compliance

A frequent and costly error made by international founders is having spelling mismatches between different corporate and personal documents. In the era of strict digital Know-Your-Customer (KYC) and Anti-Money Laundering (AML) regulations, US banks (such as Mercury, Wise, and traditional institutions) and payment processors (such as Stripe and PayPal) use automated compliance systems to verify identities. The spelling of your personal name and your company name must match exactly across all of the following documents:

- Your physical passport (which is the primary identification document for non-residents).

- The LLC's Articles of Organization approved by the Secretary of State.

- The Operating Agreement signed by the members.

- The IRS Form SS-4 and the resulting EIN Confirmation Letter (CP 575 or Form 147C).

- The bank account application.

If your passport lists your name as "João Silva", but your EIN application or Operating Agreement lists you as "Joao Silva" or "Joao G. Silva", bank compliance algorithms will flag this as a mismatch. This can lead to your application being rejected, account setup being delayed for weeks, or your account being frozen after you begin processing funds. Pay close attention to localized characters (such as Turkish "ı", "ö", "ş", "ç", Spanish "ñ", or Cyrillic/Arabic script transliterations). Ensure that the exact English characters on your passport are used across all corporate documents. A single mismatched character or a missing middle name can disrupt your banking capabilities and halt your business operations.

Operating Agreement Provisions for Single and Multi Member LLCs

An Operating Agreement is an internal, legally binding contract that outlines the financial structure, management protocols, voting rights, and operational guidelines of the LLC. Although many states do not require you to file this agreement with the state registry, creating one is absolutely essential for legal compliance, corporate governance, and financial setup. It serves as the primary governing document for the LLC, overriding default state rules that might not align with your business objectives. Disclaimer: this topic may change based on state, service provider, and current regulations.

Why Single-Member LLCs Require an Operating Agreement

Many solo entrepreneurs assume that because they are the sole owner, they do not need an agreement. This is a critical legal mistake. An Operating Agreement is required for several reasons:

- Opening Bank Accounts: Banks (such as Mercury, Wise, and retail institutions) routinely request a signed copy of your Operating Agreement to verify who has the authority to open accounts, manage corporate funds, and bind the LLC legally. Without a signed Operating Agreement, opening a business account is practically impossible.

- Preserving the Liability Shield: Having a formal agreement signed by you demonstrates to courts and tax authorities that the LLC is operated as a separate entity from your personal life, reinforcing your liability shield. If a creditor attempts to pierce the corporate veil, the Operating Agreement is key evidence showing corporate structure and separation.

- Clarifying Ownership for Audits: In the event of an IRS audit or legal dispute, the agreement serves as the official proof of your 100% ownership interest and management control. It clearly establishes that there are no other equity holders.

- Succession Planning: A single-member Operating Agreement should contain provisions detailing what happens to the LLC if the sole member dies or becomes incapacitated. Specifying a successor member avoids leaving the company in legal limbo and prevents the state from automatically dissolving it.

Multi-Member LLC Provisions: Managing Shared Ownership

When an LLC has more than one member, the Operating Agreement becomes a complex document that must address numerous operational and financial scenarios. Multi-member agreements are designed to prevent disputes and outline clear paths for resolving conflicts. A comprehensive multi-member Operating Agreement must include the following provisions:

- Capital Accounts and Contributions: The agreement must detail the initial cash, property, or services contributed by each member. It must also establish rules for capital calls, which are requirements for members to contribute additional capital in the future if the business needs funding. It should specify the consequences if a member fails to meet a capital call, such as reducing their ownership percentage.

- Allocation of Profits, Losses, and Distributions: It must define how the company's financial profits and losses are distributed among the members. While these allocations typically match ownership percentages, an LLC offers the flexibility to distribute profits disproportionately, provided there is a substantial economic effect. The agreement must also specify when and how cash distributions are made.

- Voting Rights and Decision Thresholds: The agreement must state the voting power of each member, which is usually proportional to their ownership interest. It should categorize decisions into minor day-to-day operations (which can be decided by a manager or simple majority) and major decisions (such as selling the company, taking on large debts, or admitting new members) which may require a supermajority or unanimous consent.

- Buy-Sell Provisions and Transfer Restrictions: To prevent unwanted third parties from acquiring ownership, the agreement must restrict members from selling or transferring their interests without the consent of other members. It should include a Right of First Refusal (ROFR), giving existing members the first opportunity to buy out a departing member's interest. It should also establish buyout formulas and valuation methods to determine the company's worth in the event of death, divorce, bankruptcy, or voluntary exit of a member.

- Tax Classification and Filings: By default, a multi-member LLC is classified as a partnership for federal tax purposes. The LLC must file an annual Form 1065 (U.S. Return of Partnership Income) and issue a Schedule K-1 to each member reporting their share of profits and losses. The Operating Agreement must designate a "Partnership Representative" to handle tax audits. Additionally, the agreement should note that the members can elect to have the LLC taxed as a C-Corporation (Form 1120) or, if they meet the eligibility requirements, as an S-Corporation.

- Dispute Resolution Mechanisms: In the event of a deadlock where members cannot agree on a major decision, the agreement must outline a resolution process. This can include mediation, binding arbitration, or a "shotgun clause" (where one member offers to buy the other out at a set price, and the other member must either sell their share or buy the first member's share at that same price). Outlining these procedures avoids costly court battles and keeps the business operational during disputes.

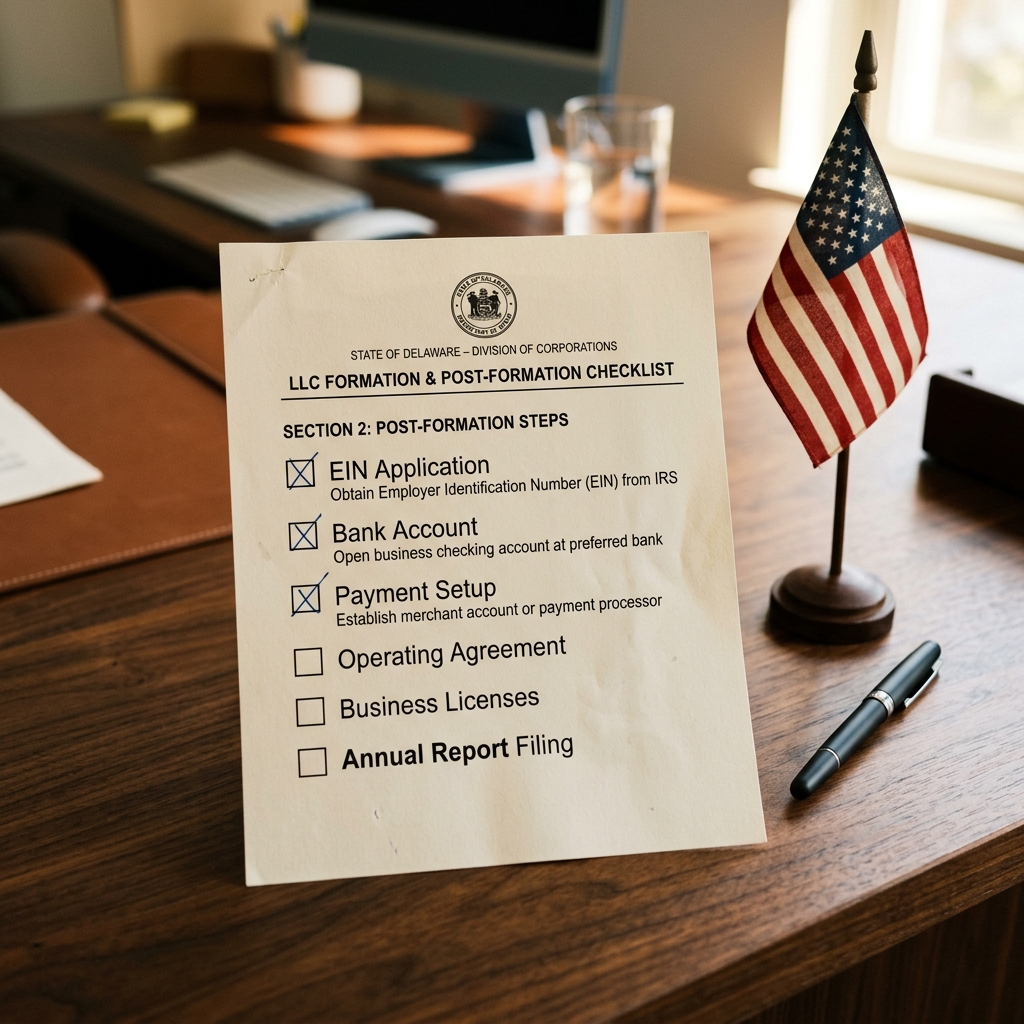

Post Formation Compliance and Federal Tax Roadmap

Registering your LLC is only the first step. To keep your company in good standing with state and federal governments, you must complete several critical post-formation steps and manage annual compliance deadlines. Operating a US business requires strict adherence to corporate and tax laws. Neglecting these requirements can lead to frozen bank accounts, personal liability, and severe financial penalties. Disclaimer: this topic may change based on state, service provider, and current regulations.

Obtaining an Employer Identification Number (EIN)

An EIN is your company's federal tax ID, issued by the IRS. You must obtain an EIN to open a US bank account, set up payment processors (like Stripe or PayPal), and file annual tax disclosures. If you do not have a US Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), you cannot apply online. Instead, you must apply for an EIN by submitting Form SS-4 to the IRS via fax or mail. The form must be completed with your LLC's legal name, state of formation, and your personal details. For non-residents, the fax number to send Form SS-4 is +1 (855) 641-6935. Once processed, the IRS will fax or mail back your EIN Confirmation Letter, known as CP 575 (or Form 147C). The processing time typically ranges from 2 to 4 weeks depending on IRS workload. This letter is the official document that banks will require to verify your corporate tax ID.

Setting Up a Commercial Bank Account

Once you have your approved state documents and your EIN, you should immediately open a dedicated US business bank account. You must never mix personal transactions with corporate funds. Since traveling to the US to open a brick-and-mortar account is difficult and expensive, most global founders use digital banking platforms like Mercury or Wise. These platforms allow 100% remote account setup. To successfully pass bank compliance checks, you must provide:

- Your approved Articles of Organization / Certificate of Formation.

- Your EIN Confirmation Letter (CP 575 or Form 147C) issued by the IRS.

- Your signed Operating Agreement proving ownership.

- A valid international passport with clear details.

- A US business virtual address (P.O. Boxes are strictly rejected by banks due to federal regulations).

- Additional documentation, such as website URLs, utility bills, or lease agreements, may be requested by the bank's compliance team to verify the nature of your business and your physical location.

Federal Tax Obligations: ETBUS vs Non-ETBUS

Understanding your US federal tax liability is crucial to avoid legal issues. For US tax purposes, a single-member LLC owned by a non-resident is classified as a "disregarded entity" by default. This means the LLC itself does not pay federal income tax. Instead, the profits flow through to the owner, who is taxed individually. For non-residents, the tax liability depends on whether the LLC is "Engaged in Trade or Business in the United States" (ETBUS). Understanding this distinction is key:

- Non-ETBUS Status: If your business has no physical presence in the US—meaning you have no offices, no warehouses, no employees, and no "dependent agents" operating in the US on your behalf—and you operate the business entirely from abroad, you are considered non-ETBUS. This applies to most digital service providers, SaaS creators, remote freelancers, and software developers. For non-ETBUS entities, your business income is considered foreign-source income. As a result, you owe 0% US federal income tax and do not have to pay US income taxes. However, you must still file annual information returns with the IRS.

- ETBUS Status: If your LLC has physical operations in the US—such as warehouses (including Amazon FBA if structured in a way that constitutes a dependent agent), employees on US soil, or exclusive agents working solely for you in the US—your business is considered ETBUS. Any income that is "Effectively Connected Income" (ECI) with the US trade or business will be subject to US federal income tax rates. In this case, you must file Form 1040-NR (Nonresident Alien Income Tax Return) and pay tax on your net US profits.

Mandatory Information Filings: IRS Form 5472 and Form 1120 pro-forma

Even if your LLC is non-ETBUS and owes 0% US tax, you are legally required to file annual information returns with the IRS. Under Internal Revenue Code Section 6038A, foreign-owned US disregarded entities must file Form 5472 (Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign-Owned U.S. Disregarded Entity). This is a disclosure form that reports "reportable transactions" between the LLC and its foreign owner, including capital contributions, profit distributions, loans, or zero-value administrative transactions. The filing requirements are strict:

- Form 5472 & Form 1120: You must complete Form 5472 and attach it to a "pro-forma" Form 1120. Form 1120 is the corporate income tax return, but for a disregarded entity, you only fill out page 1 with basic company info (name, address, EIN, and checking the foreign disregarded entity box). You do not fill out any financial sections of Form 1120; all financial reporting is done on Form 5472.

- Filing Deadline: These forms must be filed together and sent to the IRS by April 15th of the year following the tax year. They cannot be e-filed; they must be sent via physical mail or faxed to the IRS designated fax number.

- The Penalty for Non-Compliance: The penalty for failing to file Form 5472, filing it late, or submitting incomplete information is a massive **$25,000** per year. The IRS has increased enforcement of this rule, and the penalty is assessed automatically without warning. This is the single most important compliance requirement for foreign founders.

For multi-member LLCs, the tax requirements are different. The entity is taxed as a partnership and must file Form 1065 (U.S. Return of Partnership Income) by March 15th, issuing a Schedule K-1 to each partner. This is a complex partnership tax return that requires detailed bookkeeping.

State Annual Reports and Franchise Taxes

In addition to federal tax filings, you must maintain your company's active status with the state of formation by paying annual fees and filing annual reports. Failure to pay these fees will result in late penalties and the eventual administrative dissolution (forced closure) of your LLC, which destroys your liability shield. The requirements vary by state:

- Wyoming: An annual report and fee ($62) are due on the first day of the anniversary month of your LLC's formation. Wyoming does not have state franchise or income taxes.

- Delaware: A flat franchise tax ($300) must be paid on or before June 1st of every year following the year of formation. Delaware also requires you to maintain a registered agent, which costs around $50-$150 annually.

- Florida: An annual report and fee ($138.75) are due between January 1st and May 1st of every year. If you file even one day late, the state imposes an automatic, non-negotiable $400 late fee.

- New Mexico: The state does not require annual reports or annual franchise fees for LLCs. Your annual state maintenance fee is exactly $0. You only need to pay your registered agent's annual fee to keep your company in active status.

Frequently Asked Questions

Can a non-US resident own and operate a US LLC without an ITIN or SSN? ▼

Yes, absolutely. There are no citizenship or residency requirements to own or operate a U.S. Limited Liability Company (LLC). Anyone from any country (except those blacklisted by the U.S. Office of Foreign Assets Control, OFAC) can form, own 100% of, and run a U.S. business entity from anywhere in the world. You do not need a U.S. Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN) to register the LLC or to obtain an Employer Identification Number (EIN) for your business. The registration and operational processes can be managed completely online. Disclaimer: this topic may change based on state, service provider, and current regulations.

How do non-US residents obtain an EIN and how long does it take? ▼

Non-U.S. residents who do not have an SSN or ITIN cannot apply for an EIN online. Instead, they must apply by filing Form SS-4 (Application for Employer Identification Number) with the IRS via fax or mail. The process involves filling out the form with your LLC's legal name, state, and your personal details as the "responsible party." You then fax this form to the IRS at +1 (855) 641-6935. The IRS will process the application and fax back the EIN confirmation letter (CP 575 or Form 147C). The processing time is typically 2 to 4 weeks, depending on the IRS backlog. It is important to fill out the form accurately, as any errors can result in immediate rejection, restarting the waiting period. Disclaimer: this topic may change based on state, service provider, and current regulations.

What is the difference between ETBUS and Non-ETBUS tax status for foreign owners? ▼

The distinction between ETBUS (Engaged in Trade or Business in the United States) and Non-ETBUS determines whether you owe US federal income taxes. If your LLC is a single-member disregarded entity and has no physical presence in the US—no offices, no warehouses, no employees, and no "dependent agents" (meaning exclusive agents working solely for you in the US)—you are classified as Non-ETBUS. Your income is considered foreign-source income, and you owe 0% US federal income tax. Conversely, if you have a physical office, hire employees, or have a dependent agent in the US, your company is considered ETBUS. Any income effectively connected with your US business operations (ECI) will be taxed at standard US corporate or individual tax rates, and you must file a U.S. tax return. Disclaimer: this topic may change based on state, service provider, and current regulations.

What are IRS Form 5472 and Form 1120 pro-forma, and what happens if I fail to file them? ▼

Form 5472 is an annual information return required by the IRS for foreign-owned single-member LLCs (which are treated as disregarded entities). It is used to report "reportable transactions" (such as capital contributions, distributions, or loans) between the LLC and its foreign owner. Even if the LLC has no activity or has zero profits, a Form 5472 must still be submitted. It must be attached to a "pro-forma" Form 1120 (where only basic company identifiers are filled on page 1). The deadline to file is April 15th of each year. Failure to file, filing late, or submitting incorrect or incomplete details carries an automatic and non-negotiable **$25,000** penalty per year. This is a federal compliance requirement that the IRS strictly enforces, making it critical for foreign founders to complete. Disclaimer: this topic may change based on state, service provider, and current regulations.

Why do New York and Nebraska have publication requirements, and should I avoid them? ▼

Both New York and Nebraska have outdated laws requiring newly formed LLCs to publish notices of their formation in newspapers. In New York, under LLC Law Section 206, you must publish a notice in two county-clerk-designated newspapers for six consecutive weeks, which costs between $600 and $1,500 depending on the county. Nebraska law Section 21-117 requires three consecutive weeks of publication in a legal newspaper. Once published, you must file a certificate of publication with the state. Failure to publish in NY within 120 days suspends the LLC's authority to do business. Because of the high costs and logistical difficulties of managing newspaper publication from abroad, international founders should avoid forming LLCs in NY and Nebraska unless they have a physical operations center there. Choosing states like Wyoming or New Mexico bypasses these expensive and complex processes. Disclaimer: this topic may change based on state, service provider, and current regulations.

Can I open a U.S. bank account remotely, and what documents are required? ▼

Yes, you can open a U.S. business bank account completely remotely using digital banking platforms such as Mercury, Wise, or Payoneer. Opening accounts at traditional physical retail banks (like Chase or Bank of America) usually requires traveling to the U.S. in person. To open a remote digital account, you must present your approved Articles of Organization, your IRS EIN Confirmation Letter (CP 575 or Form 147C), your signed Operating Agreement, and a valid international passport. You must also provide a valid U.S. physical business mailing address (not a P.O. Box). Bank compliance teams will verify all names and details. Any spelling mismatch between your passport name and company documents can result in immediate rejection of your application. Disclaimer: this topic may change based on state, service provider, and current regulations.

Why does the spelling of my name and my company name need to match my passport exactly? ▼

U.S. banks and payment processors operate under strict federal KYC (Know Your Customer) and AML (Anti-Money Laundering) regulations. When you apply for a financial account, their automated systems cross-check database records. If your passport spelling is "Marta Sánchez" but your corporate filing or EIN application says "Marta Sanchez" or "Marta S. Sanchez", the system will flag the mismatch. Even minor differences like using a Turkish "ı" instead of an "i" or a missing middle name can trigger compliance alerts. Mismatches lead to application rejections, account suspension, or funds being frozen. You must ensure that every corporate document, operating agreement, and IRS form matches the exact English characters of your passport name. Disclaimer: this topic may change based on state, service provider, and current regulations.

What are the annual state fees and maintenance obligations for Wyoming, Delaware, Florida, and New Mexico? ▼

Annual obligations vary significantly by state. Wyoming requires a $62 annual report fee due on the first day of your LLC's anniversary month. Delaware requires a flat $300 franchise tax due by June 1st of each year, plus registered agent fees. Florida has an annual report fee of $138.75 due by May 1st, and missing this deadline results in an automatic, non-negotiable $400 late fee. New Mexico has no annual report requirements and a $0 annual state maintenance fee. If you fail to file reports or pay state fees, the state will place your LLC in delinquent status and eventually dissolve it administratively, destroying your liability shield and making you personally liable. Disclaimer: this topic may change based on state, service provider, and current regulations.

Is an Operating Agreement legally required for a single-member LLC, and is it filed with the state? ▼

An Operating Agreement is not filed with the Secretary of State, meaning it is a private internal document. However, it is legally required in practice. Without it, you cannot open a corporate bank account, as U.S. banks demand to see a signed agreement to verify who has authority to open and manage accounts. Additionally, having a signed Operating Agreement is vital to maintaining your liability shield. It proves to courts, creditors, and the IRS that your LLC is a separate legal entity and not just a personal alter ego. A comprehensive agreement should detail capital contributions, distribution of profits, sole member control, and succession plans. Disclaimer: this topic may change based on state, service provider, and current regulations.